NEWS FLASH- book and course Custodians and Earth Custodians (Vision For Caring For Our Earth’s Ecosystem) are available . SEE- Main Menu: Custodians

Fraser Institute reports of the perceived most and least favourable mining industry jurisdictions 2019

One of the outcomes of the PDAC annual confere nces is a review of the mining industry. This review is an assessment of the most and least prospective jurisdictions to explore and develop resources. This review is undertaken by the Fraser Institute an independent Canadian public policy research and educational organisation. Fraser Institute has offices in Vancouver, Calgary, Toronto, and Montreal and ties to a global network of think-tanks in 87 countries. In 2019 Fraser Institute denoted Western Australia as the most attractive global jurisdiction to explore and develop a resource. for mining investment followed by Finland (2nd), the U.S. state of Nevada (3rd), based on its Annual Survey of Mining Companies.

Based on 76 jurisdictions ten most attractive 1) Western Australia 2) Finland 3) Nevada 4) Alaska 5) Portugal 6) South Australia 7) Republic of Ireland 8) Idaho 9) Arizona 10) Sweden

The 10 least attractive regions are: 67) Nicaragua 68) Mali 69) Democratic Republic of Congo (DRC) 70) Venezuela 71) Zambia 72) Dominican Republic 73) Guatemala 74) La Rioja, Argentina 75) Chubut, Argentina 76) and Tanzania 77)..

2020

The top jurisdiction in the world for investment based on Investment Attractiveness Index is Nevada, which moved up from 3rd place in 2019. Arizona, which ranked 9th in 2019, moved into 2nd place. Saskatchewan climbed eight spots from 11th in 2019 to 3rd in 2020. Western Australia ranked 4th this year after topping the ranking last year, and Alaska dropped a spot from 4th in 2019 to 5th in 2020. Rounding out the top 10 are Quebec, South Australia, Newfoundland & Labrador, Idaho, and Finland.

When considering both policy and mineral potential in the Investment Attractiveness Index, Venezuela ranks as the least attractive jurisdiction in the world for investment followed by Argentina: Chubut, and Tanzania. Other jurisdictions in the bottom 10 (beginning with the worst) are Indonesia, Argentina: La Rioja, Bolivia, Argentina: Mendoza, Zimbabwe, Spain, and Michigan.

Geological potential and economic considerations are important factors in mineral exploration that must be considered with a region’s policy climate. The Fraser Institute uses a Policy Perception Index (PPI) composite measure of the overall policy attractiveness of the 77 jurisdictions in their survey. The Policy Perception Index is composed of survey responses to policy factors that affect investment decisions for exploration and mining. These policy factors include uncertainty on the effective administration of current regulations, environmental regulations, regulatory duplication and the prevailing legal system and taxation regime. Other administrative uncertainties include protected areas, disputed land claims, infrastructure, socioeconomic and community development conditions, trade barriers, political stability and labour regulations. The quality of the geological database is also in doubt as is security in operation and the skill level and availability of labour

Current ratings on the PPI score has Idaho displacing Finland for top spot with the highest PPI score of 100. This was followed by Wyoming in the second place, which moved from 16th in the previous year. The other top 10 rankings are Finland, the Republic of Ireland, Nevada, Utah, Arizona, Newfoundland & Labrador, Saskatchewan, and New Mexico.

The 10 least investment attractive jurisdictions based on the PPI rankings are Venezuela (least attractive), Argentina: Chubut, Zimbabwe, Bolivia, Argentina: Mendoza, Tanzania, Papua New Guinea, the Democratic Republic of Congo (DRC), Indonesia, and Argentina: La Rioja.

2021

Fraser Institute’s 2021 annual mining and exploration company survey assesses how mineral endowments and public policy factors such as taxation and regulatory uncertainty affect exploration investment. The survey had 290 responses (13%) providing data to evaluate 84 jurisdictions increasing from 77 in 2020, 76 in 2019, 83 in 2018, and 91 in 2017. The number of jurisdictions that can be included in the study is related to the size of the sector, global commodity prices and other factors. This survey also includes permit times, similar to 2020.

The Investment Attractiveness Index

The Investment Attractiveness Index combines the Best Practices Mineral Potential index based on their geologic attractiveness, and the Policy Perception Index. Investment attractiveness is a composite index that measures the effects of government policy on exploration investment. Measuring the attractiveness of a jurisdiction is based on policy factors such as onerous regulations, taxation levels, the quality of infrastructure, and the other policy related questions. The Policy Perception Index alone does not recognize the fact that investment decisions are often based mainly on the pure mineral potential of a jurisdiction. Overall, respondents consistently indicate that approximately 40 percent of their investment decision is determined by policy factors.

Highest Investment attraction Index.

The top global jurisdiction for investment based on the Investment Attractiveness Index is Western Australia, which moved up from 4th place in 2020. Saskatchewan went up from a rank of 3rd in 2020 to 2nd in 2021. Nevada, which topped the ranking last year, ranked 3rd in 2021. Rounding out the top 10 are Alaska, Arizona, Quebec, Idaho, Morocco, Yukon, and South Australia. The United States has the most jurisdictions (4) in this year’s top 10, followed by Canada (3), Australia (2), and Africa (1).

Lowest Investment Attraction index

When considering both policy and mineral potential in the Investment Attractiveness Index, Zimbabwe ranks as least attractive jurisdiction for investment followed by Spain, the Democratic Republic of Congo (DRC), and Mali. Also, in the bottom 10 (from the next worst) are Nica ragua, China, Panama, Mendoza, Venezuela, and South Africa. Latin America (including Argentina and the Caribbean) and Africa are the regions with the greatest number of jurisdictions (4) in the bottom 10. Asia, which features once again in our analysis for the first time since 2018, and Europe, both contribute with one jurisdiction each in the bottom 10.

Top Policy Perception Index jurisdictions

The policy perception Index is “report card” to governments on the attractiveness of their mining policies. Geologic and economic considerations are important factors in mineral exploration however, a region’s policy climate is also an important investment consideration. The Policy Perception Index (PPI) composite index measures the overall policy attractiveness of the 84 jurisdictions in the survey. The index is composed of survey responses to policy factors that affect investment decisions. Policy factors examined include uncertainty concerning the administration of current regulations, environmental regulations, regulatory duplication, the legal system and taxation regime, uncertainty concerning protected areas and disputed land claims. Also included are infrastructure, socioeconomic and community development conditions, trade barriers, political stability, labour regulations, quality of the geological database, security, and labour and skills availability.

The Republic of Ireland with the highest PPI score of 100 displaced Idaho (which dropped out of the top 10) this year . Morocco with a score of 98.06 took the second and displaced Wyoming, which also dropped out of the top 10 . Other top 10 ranked jurisdictions are Northern Ireland, Western Australia, Quebec, Nevada, Utah, Saskatchewan, Finland, and Alberta. Europe and Canada are the regions with the most jurisdictions (3 each) in the top 10 followed by the United States (2), Australia (1), and Africa (1).

The bottom policy perception Index jurisdictions

The 10 least attractive jurisdictions for investment based on the PPI rankings are Venezuela, (last) Philippines, Argentina: Chubut, Nicaragua, y: Mendoza, Zimbabwe, the Democratic Republic of Congo (DRC), Bolivia, Kyrgyzstan, and Mongolia. This year, Latin America and Argentina contribute five of the bottom 10 jurisdictions followed by Africa (2), Asia (2), and Oceania (1).

For your assessment of jurisdictions in Queensland, Papua New Guinea and Mongolia.

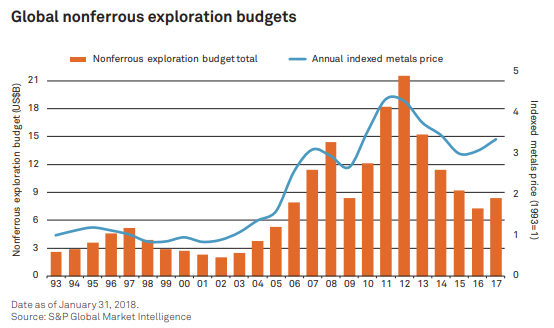

major miners (revenues >US$1 billion) allocated only a small proportion of revenues to exploration with riskier exploration remaining relatively unattractive.

major miners (revenues >US$1 billion) allocated only a small proportion of revenues to exploration with riskier exploration remaining relatively unattractive.